Will Fintechs make banks obsolete? Will we still use banks in 10 years? Are banks going to disappear?

These are questions we love to ask in the Fintech world. Yet most of us agree that banks are not going to disappear, and that there is a place in the future for both Fintech companies and banks. Yet, there is no denying that Fintech is turning heads. According to a KPMG survey, 56% of bankers see Fintech as the biggest disrupter of financial institutions, 90% now have some sort of Fintech strategy in place with 75% of them focusing on enhancing customer experience. Obviously, Fintech is ruffling some feathers - but how?

Here are four main ways Fintech is disrupting banking:

1. Customer-first mindset

It’s very interesting to compare how banks release products with how Fintech companies release products. Incumbent banks keep adding new features and implementing advanced technology. They add an interest rate that increases with the number of steps you take, or free co-working spaces in the middle of the city. They add a cool feature for their customers, integrate it into the plan, build it, and then market it. Only once the product is built do they move to the “marketing” part. “We’ve created this snazzy feature, now we need to figure out how to get more people to use it.” This approach is called “product-first”. I’m not saying this is necessarily a bad approach, just that this is how things are usually done in the banking world.

Fintech startups and banking technology companies are taking a different approach: “customer first”. They put themselves in the position of the customer and completely reimagine the customer journey. The customer doesn’t think “I want a mortgage”, they think “I want a bigger house”. 🏡 They don’t care about the fancy tech that you’re using, they just want something that works and delivers what they need. This is disruptive because it’s a new way of thinking.

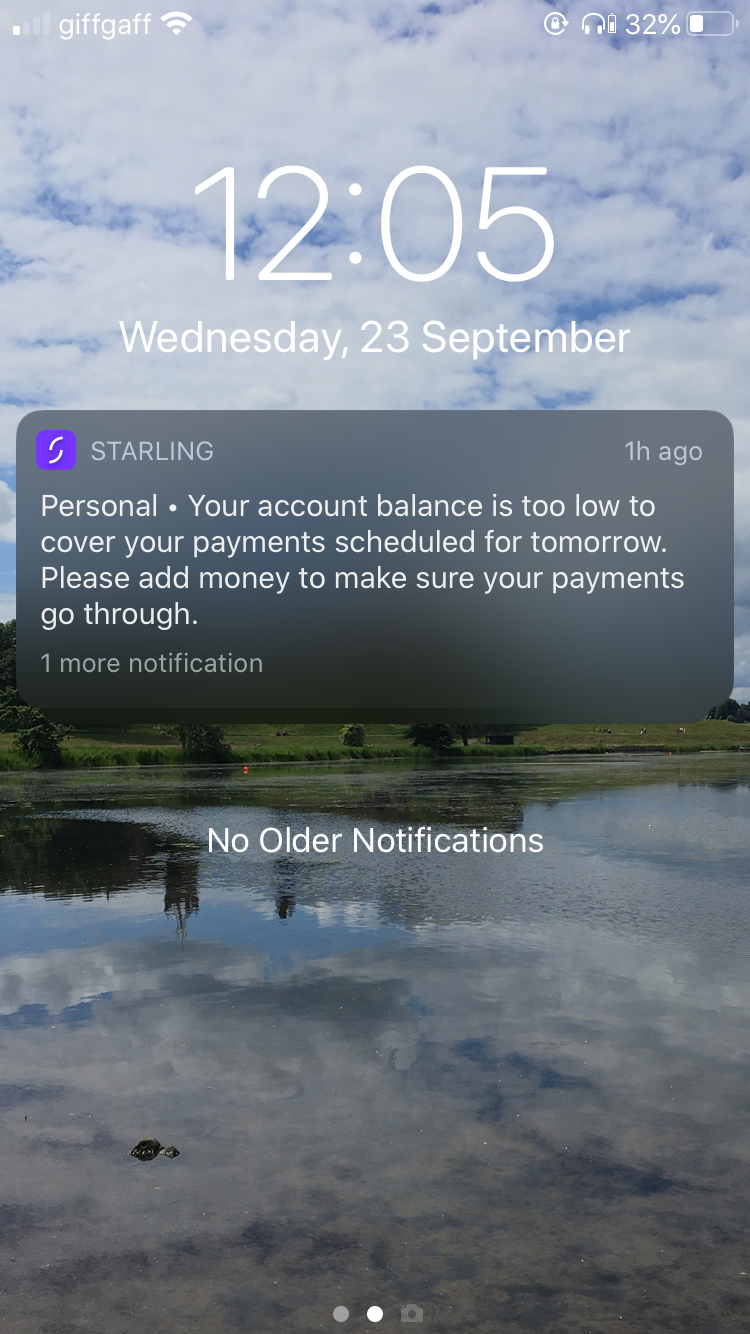

A perfect example is overdraft charges. When surveyed, most bank customers (68%) would rather have their bank decline a payment than pay an overdraft fee. But of course, a bank would rather increase profit and shareholder value, so they charge an expensive overdraft. The bank is not customer-centric. If it were, it wouldn’t charge huge overdraft fees. This is different to modern neobanks, who will warn me the day before if I don’t have enough funds to pay by direct debit:

Sure, most customers use these neobanks as a secondary or third account. But it still means that Monzo, Revolut and Starling are getting the day to day data on my spending. What does my incumbent bank see? “Deposit to Monzo”, “mortgage payment”. Fintechs are getting the real data, while incumbents are becoming more and more the boring old “pipes”. The more daily spending data the neobanks gather, the more personalised my bank account can be. In the future, it’s the companies and banks with the best data analytic capabilities that will win. More on this later. 👇

Most incumbents’ marketing is about why their product is better than others. With Fintech, it’s just about simplifying banking and serving real customer needs. Banks are selling banking products, Fintechs are servicing customers. Just by focusing on doing one thing brilliantly that banks do badly - being customer first - Fintechs are disrupting banking.

2. Faster execution

Another way Fintech is disrupting banking is with its startup business model, mindset and culture. While banks employ hundreds of thousands of employees, many Fintechs just have a few hundred. While some banks have been around for decades, most Fintechs are under 10 years old. While most Fintechs embrace technology, banks are overcoming legacy infrastructure.

Banks have many more responsibilities, stakeholders and capital to operate with; they need to stay up to date with hundreds of regulations and meet new compliance laws. Banks spend a whopping 73% of their budget just on maintenance. This is very different from startups, which build features quickly and efficiently and don’t need to meet as many regulatory requirements (because they don’t hold a banking license). The server is on the cloud and the tech infrastructure is up to date. They’re 70% cheaper to market and it costs them $1 to $38 to acquire a customer - compared to $200 for traditional banks.

Just look at what DBS did in order to engage in digital transformation: they had to adopt a startup mindset. As the CEO, Piyush Gupta, says in the case study, DBS had to focus on running experiments. He explains that “everybody was reimagining how you could do things”. This meant mini hackathons, new training and smaller teams. The culture and mindset of a startup make it easier to add value, build and ship products.

It’s a lot harder to innovate and ship products quickly as a large incumbent bank. Fintech companies have the advantage of being smaller, nimbler and tech-savvy. This is what makes them disruptive in a world that is only going to become more dependent on technology.

3. Focus on partnerships and connections

In the book Bank 4.0, Brett King describes how an Australian bank spent months in talks of collaborating with his neobank, Moven. They would ask him all sorts of questions trying to take in as many technical details about how the neobank worked, the features, the partners and the objectives. The talks went on for nearly 3 years, and it was soon obvious that they had no intention of partnering up. In 2015, they then proceeded to spend $20 to $30 million to launch their own “financial wellness” app. It cost them two years and over $20 million to launch their own product, when they could have partnered with Moven, launched in 3 months and spent under $1 million. 🤷♀️

The point is, banks shouldn’t believe they need to build everything themselves. The future is partnerships, APIs and Banking as a Service. Fintech is disruptive because it’s all about integration: they specialise in doing one thing very well, then connecting with everyone else.

Truelayer allows any company to get into financial services. Onfido makes it easy to implement online KYC. Moov allows companies to store, receive and send payments.

As Chris Skinner says repeatedly, Fintech is like building Lego blocks: each piece fits together nicely and builds on top of each other. Incumbent banks are spaghetti: the departments are siloed, the infrastructure uses a mix of old and new programming languages and mergers and acquisitions aren’t completely integrated. We’re moving towards a world of embedded payments, software as a service and Open Banking. Those that specialise and partner up will succeed. Those that try to do everything themselves will get acquired. If this is a topic that fascinates you as much as it fascinates me, I recommend reading a summary I wrote about the huge advances of Ant Financial in China.

Fintechs are disrupting banking because they focus on doing one thing well and then partnering up with others. Banks are still trying to build everything themselves, which means they lag behind, are slow to compete and waste money and energy on unnecessary projects.

4. Real digital transformation

Finally, the word that’s constantly on the tip of everyone’s tongue: digital transformation.

Fintechs are disrupting banking because they are adopting a tech-first mindset. Technology is an essential part of what they do. Banks treat technology as a project: they hire a “Chief Digital Officer” to design a banking app and then say: “We’ve done technology, we built an app”. Nope, that’s not digital transformation.

Digital transformation is very much linked to the customer first mindset. That’s because technology has put people in control: they now have options, they can now do their own research, they can read reviews and decide which bank/insurance company/financial product to buy for themselves. So how can we use technology to best serve our customers?

One example is Ant Financial’s approach: they have everything integrated into their own ecosystem. Want to rent a flat but can’t afford the deposit? Build your Zhima Credit score, use their own property platform and they’ll waive your deposit. Need a loan for your new shop? With Ant Financial you can apply in 3 minutes, receive the money in 1 second and 0 manual intervention. This is just an example - I am aware there are many downsides to Ant Financial’s approach and that we should take it all with a pinch of salt. But we can’t deny that what they’ve done with technology and finance is quite impressive.

Chris makes the analogy that banks are trying to make faster horses, while TechFins and Fintechs are trying to make cars. Building cars requires a complete rethinking of the business model and how we serve our customers. What if we could wear glasses that immediately told us if we could afford an item in a shop as we looked around? Or if we didn’t have to take our wallet or phone to dinner anymore - the cameras would identify us and we could pay with our identity? Or micro-loans with minimal rates for any item that is worth paying upfront (like an annual train pass)?

The good news is that incumbent banks can do digital transformation. In my article on how DBS and BBVA approached transformation, we see how Piyush took on the challenge of digital transformation and turned DBS into the first bank to demonstrate a link between digitisation and shareholder value. It took them nearly a decade, several phases of development and a huge shift in culture, but they did it.

The other thing to mention is data. The companies and banks that figure out how to gather and structure data to make better decisions will come out winning. But if you still can’t tell that your mortgage and business customer is the same person, how can you make better decisions? If you still need a wet signature to create an account, how are going to encourage more people to sign up?

In 10 years, the competition will be about data analytics - the only way to distinguish yourself will be through digital customer interaction. Digital transformation isn’t just a buzzword, it’s something that has to happen. Fintechs are embracing it, most (not all) banks are not. That’s why Fintech is disrupting banking.

These are four of the main ways I believe that Fintech is disrupting banking. As many will say, this is not a zero sum game: Fintech companies don’t need to push out the banks. In fact, it’s the opposite: both Fintechs and banks win if they collaborate and work together. Banks have the reputation, regulatory experience and customer base, Fintechs have the culture, fast execution and facility to experiment. Although Fintech is disrupting banking, it’s by bringing these two together that we’ll get the best banking services overall.